The same, just different

You can subscribe to receive these notes by email here

The reduced frequency of these notes over the past few weeks has been due to my being on the road in New Zealand and Singapore, my first trip back since the pandemic. The long flights provided ample opportunity to reflect on my conversations and observations. So this note provides my take on some observed similarities and differences between Europe and Asia.

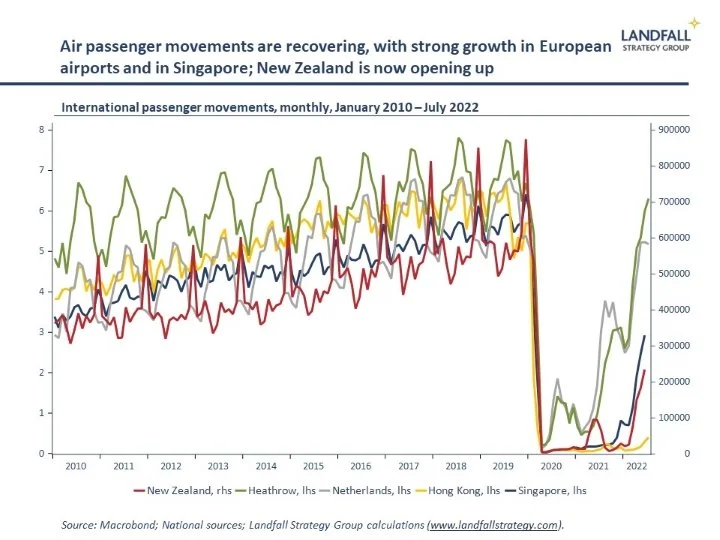

Airports, Covid, & the recovery

One clear difference, evident before departure, was the functioning of airports! Arriving at Schiphol well before 7am, I encountered snaking queues already forming outside the short-haul terminal. I was fortunate: it only took a couple of hours to get through. But the labour market stresses in a strongly rebounding European economy were clear.

In contrast, Singapore’s Changi Airport was its usual paragon of efficiency. And New Zealand airports were quiet, partly because borders hadn’t yet fully reopened.

The second obvious difference was policy approaches to Covid. Although infection rates in Singapore and New Zealand remain relatively low, mask-wearing is ubiquitous – including outdoors in tropical Singapore. Not having seen a mask in the Netherlands for a long time, it was jolting to see the ongoing reality of Covid precautions in Asia.

The tough approach in Asia to initial Covid management casts a long shadow – while Europe has continued its relatively liberal approach. There are clear differences in national risk tolerance with respect to Covid, which will have impacts on economic behaviour.

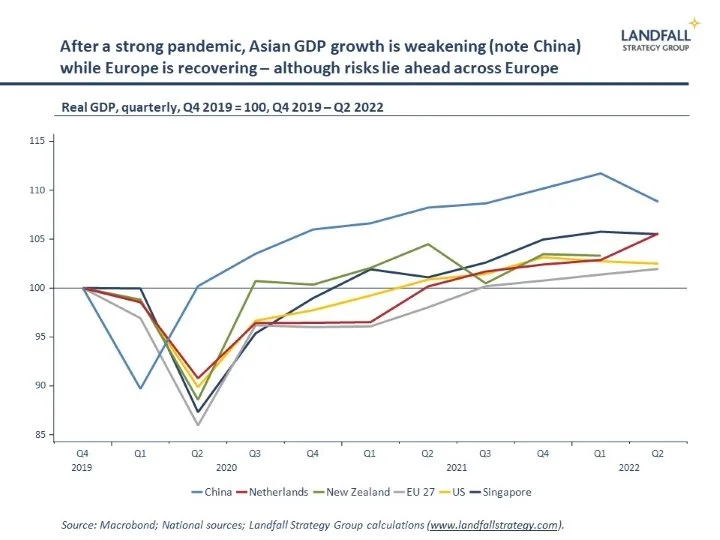

Indeed, a third striking difference between Asia and Europe is the state of the economic recovery from Covid. Asian economies performed strongly through the pandemic – partly because strong initial Covid control measures allowed them to reopen relatively quickly. Many (larger) European economies did not do as well.

But now there is some faltering in Asian economies. Singapore reported negative qoq GDP growth in Q2, and the Reserve Bank forecasts weak GDP growth in New Zealand from late 2022. A weakening Chinese economy weighs on the outlook across Asia. In contrast, European GDP numbers for Q2 were surprisingly robust – although the economic outlook in Europe is clearly clouded by high energy prices.

Geopolitics & inflation

But beyond these differences, the conversations with policy-makers, investors, and business leaders were strikingly similar in focus to those I have in Europe. Two topics that headlined almost every conversation were growing geopolitical tensions; and the economics and politics of surging inflation.

Geopolitics

The debate in Europe is dominated by the direct and indirect impact of Russia’s invasion of Ukraine. Previous notes have described the altered geopolitical landscape and different national decision-making: the expansion of NATO, commitments to increase military spending, and tough sanctions on Russia. Economic and energy relations with Russia have structurally changed – leading to substantial near-term cost in terms of higher energy prices.

It is possible that public opinion will weaken over the next several months, as high energy prices persist into the Northern winter months. But my sense is that support for Ukraine (and sanctions on Russia) across European countries will be sustained – and certainly by the US, the dominant provider of financial and military support to Ukraine.

The complacency that many European countries had with respect to geopolitics has been diminished. Indeed, there is much greater caution by European governments and firms with respect to China: it is seen as a strategic competitor not just a large market. The tone of the European debate is converging to that in Asia, where it is broadly recognised that geopolitical realities shape the ability to pursue economic engagement.

The geopolitical preoccupation in Asia over the past fortnight has been Taiwan, on the back of Ms Pelosi’s visit. Once the news of her proposed visit had leaked, it became politically difficult to back down. But the level of tension around Taiwan has been structurally increased as a consequence of her visit, even beyond that due to China’s increasingly aggressive behaviours.

China’s prolonged live fire exercises around Taiwan are likely to be seen more often, and the US is also likely to become more assertive in various ways. It is likely that there will be more frequent episodes of elevated tension around Taiwan, with associated economic costs.

Although a military conflict seems unlikely in the near term (Russia’s problems in Ukraine are cautionary for China), the chance of a mistake or a miscalculation has increased: Singapore’s Deputy PM Wong talked during the week of the dangers of ‘sleepwalking into conflict’. A military/economic conflict involving China and the West would be a much more serious matter than Russia’s invasion of Ukraine, with catastrophic economic and political consequences. Geopolitical risks topped PM Lee’s National Day Message last week.

Although the specific focus of geopolitical concern varies across regions, there is a shared sense that countries and firms need to grapple with a more geopolitically challenging context. And that choices will need to be made as the global system fragments.

Indeed, there has been some recent toughening of rhetoric in New Zealand on geopolitical issues: sanctions on Russia, tougher on China (Pacific, Taiwan), and a more Western-aligned stance. There are even rumours about New Zealand joining AUKUS, although this seems distinctly unlikely in the near-term.

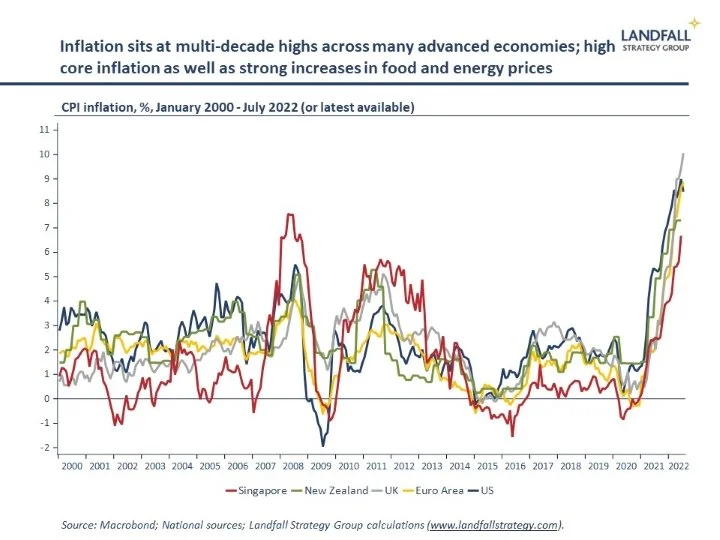

Inflation

Inflation has surged to multi-decade highs across advanced economies for a variety of reasons: excess demand, supply-side constraints, high energy and food prices, and so on. This is true in Asia as in Europe, even if inflation rates are slightly more muted in Asia (partly because Asian economies are less exposed to higher energy prices, particularly gas).

‘Happy families are all alike; every unhappy family is unhappy in its own way’, Leo Tolstoy (Anna Karenina)

Central banks in Singapore and New Zealand have tightened monetary policy in response. Indeed, on Wednesday, the RBNZ lifted policy rates by 50bp with more expected. The ECB has started to lift the policy rate but this will be a much more gradual process (partly constrained by high public debt levels in countries like Italy and Greece).

Inflation matters not simply because it can be economically damaging (demand destruction, the need for higher interest rates) but also because high inflation can impose political costs. After decades of relatively modest (and sub-target) inflation, households have rapidly acquired a distaste for resurgent inflation. Even when some of the inflation is due to external forces (such as higher energy prices), this is seen as a marker of the competence of the government’s economic management.

Governments across Asia and Europe are scrambling to deploy policy measures that will offset or control inflation: from household energy subsidies to various price controls. And countries like Singapore are also acting to strengthen the functioning of labour markets, in order to ease skills shortages – as I noted recently, labour market disruptions in the post-Covid global economy are one underlying cause for high inflation.

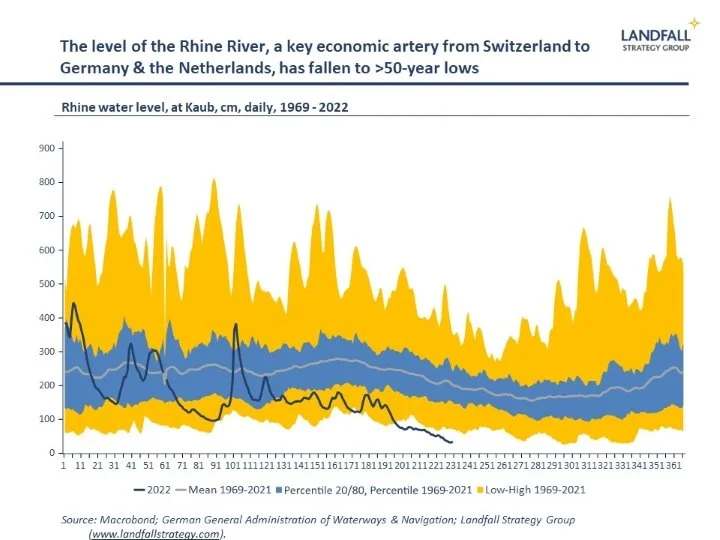

Climate records

As a final observation, while Europe experienced one of its hottest and driest summers on record (with the Rhine at historic lows), much of New Zealand experienced its wettest July on record. Although I dodged the worst of the torrential New Zealand rain, a return to a parched, brown Netherlands provided a reminder of the changing climate across the globe.

If you are not subscribed yet and would like to receive these small world notes directly by email, you can subscribe here:

We provide insights and advisory services to firms, investors, and governments on responding to global economic and geopolitical dynamics. Please do get in touch with me at contact@landfallstrategy.com if you would like to discuss how we can support you.

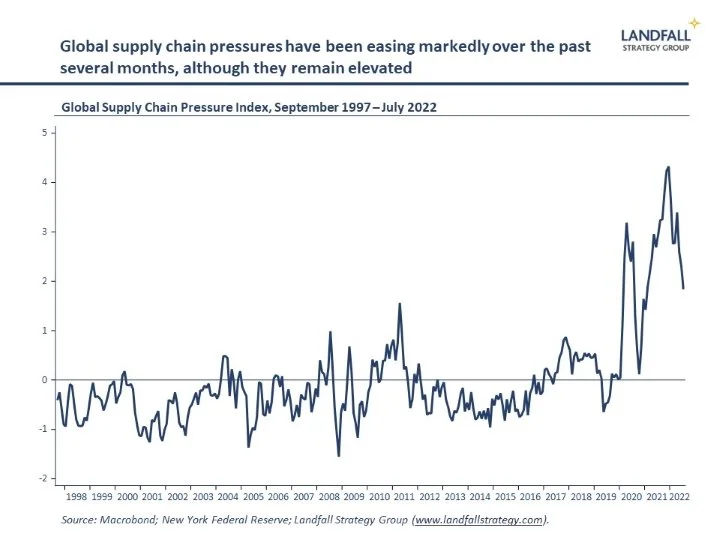

Chart of the week

Global supply chain pressures have been weakening sharply over the past several months, according to a composite measure produced by the New York Federal Reserve. International shipping congestion and delays at ports are well down, as are shipping and air freight costs. Some of the post-Covid disruptions are easing, together with a contribution from a slowing global economy. Over time, this will exert some downward pressure on inflation.

Dr David Skilling

Director, Landfall Strategy Group

www.landfallstrategy.com

www.twitter.com/dskilling